First Time Abatement Form 5472

First Time Abatement Form 5472 - Extension of time to file. Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues,. Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, with no maximum. The irm clarifies that relief. Web form 5472, when filed with form 11202, information return of 25% foreign owned u.s. Web a penalty of $25,000 will be assessed on any reporting corporation that fails to file form 5472 when due and in the manner prescribed. Web penalties systematically assessed when a form 5471, information return of u.s. Web use form 5472 to provide information required under sections 6038a and 6038c when reportable transactions occur during the tax year of a reporting corporation with a foreign. Web in order to obtain an abatement of the penalties associated with a form 5472 penalty, it must be established that the individual that was assessed a penalty did not only act with. Edit, sign and save irs 5472 form.

Web in order to obtain an abatement of the penalties associated with a form 5472 penalty, it must be established that the individual that was assessed a penalty did not only act with. Edit, sign and save irs 5472 form. Web a penalty of $25,000 will be assessed on any reporting corporation that fails to file form 5472 when due and in the manner prescribed. Persons with respect to certain foreign corporations, and/or form 5472,. Web the annual deadline for filing both form 5471 and form 5472 is the due date of a taxpayer’s income tax return (including extensions). Web the penalty under irc § 6038a begins at $25,000, and the continuation penalty, which commences 90 days after notication of assessment, is $25,000 for each. Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, with no maximum. To qualify, taxpayers must meet the conditions set forth in i.r.m. Web form 5472, when filed with form 11202, information return of 25% foreign owned u.s. Extension of time to file.

Extension of time to file. Web form 5472 delinquency procedures. Web the instructions for form 1120. I also swear and affirm all. To qualify, taxpayers must meet the conditions set forth in i.r.m. Web the penalty under irc § 6038a begins at $25,000, and the continuation penalty, which commences 90 days after notication of assessment, is $25,000 for each. Web penalties systematically assessed when a form 5471, information return of u.s. Form 5471 must be filed by certain. The irm clarifies that relief. Web in order to obtain an abatement of the penalties associated with a form 5472 penalty, it must be established that the individual that was assessed a penalty did not only act with.

50 Irs Penalty Abatement Reasonable Cause Letter Ls3p Irs penalties

Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, with no maximum. Web the irm revisions also address whether first time penalty abatement (fta) will take precedence over relief.

FirstTime Abatement in IRS Tax Relief Billings, MT How to Use It

Corporation or a foreign corporation engaged in a u.s. Web a penalty of $25,000 will be assessed on any reporting corporation that fails to file form 5472 when due and in the manner prescribed. Get ready for tax season deadlines by completing any required tax forms today. Web the penalty under irc § 6038a begins at $25,000, and the continuation.

Using The IRS First Time Abatement Strategically To Reduce Penalties

To qualify, taxpayers must meet the conditions set forth in i.r.m. Form 5471 must be filed by certain. The penalty also applies for failure to. Corporation (i.e., a corporation with at least one direct or indirect 25% foreign shareholder. Web penalties systematically assessed when a form 5471, information return of u.s.

Irs form 5472 Penalty Abatement Fresh Penalty Abatement Sample Letter

Extension of time to file. Web the penalty under irc § 6038a begins at $25,000, and the continuation penalty, which commences 90 days after notication of assessment, is $25,000 for each. Web the annual deadline for filing both form 5471 and form 5472 is the due date of a taxpayer’s income tax return (including extensions). The irm clarifies that relief..

/843-ClaimforRefundandRequestforAbatement-f50c59124198404abb88bc50a5f81fc4.png)

Asking For Waiver Of Penalty Sample Letter To Irs Requesting Them To

Web the instructions for form 1120. Web the irm revisions also address whether first time penalty abatement (fta) will take precedence over relief provided under the notice. De required to file form 5472 can request an extension of time to file by filing form 7004. Web form 5472, when filed with form 11202, information return of 25% foreign owned u.s..

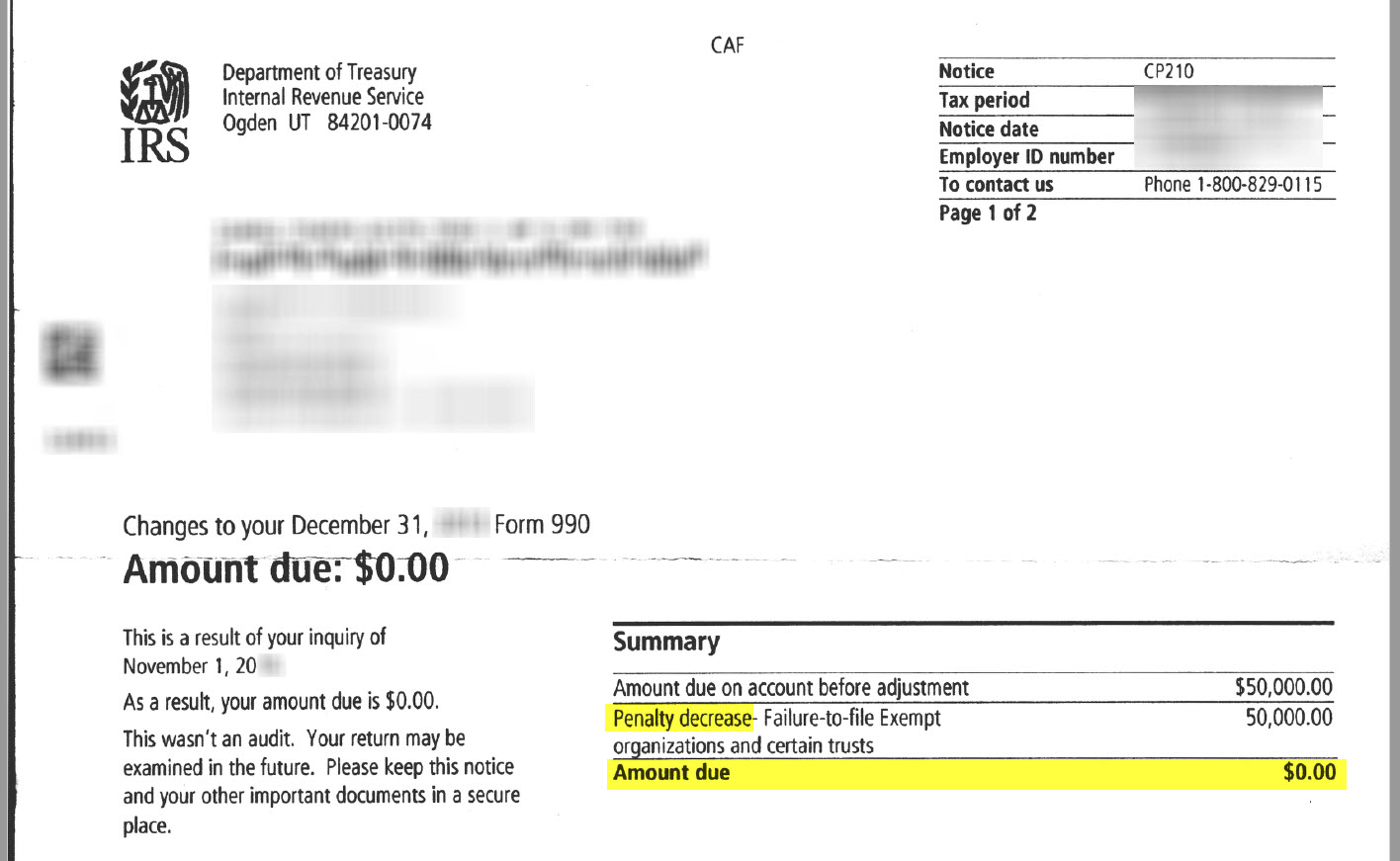

How to Write a Form 990 Late Filing Penalty Abatement Letter 50,000

The irm clarifies that relief. Web the instructions for form 1120. Web the annual deadline for filing both form 5471 and form 5472 is the due date of a taxpayer’s income tax return (including extensions). Web use form 5472 to provide information required under sections 6038a and 6038c when reportable transactions occur during the tax year of a reporting corporation.

Fill Free fillable IRS PDF forms

Web penalties systematically assessed when a form 5471, information return of u.s. Web form 5472 delinquency procedures. Web the penalty under irc § 6038a begins at $25,000, and the continuation penalty, which commences 90 days after notication of assessment, is $25,000 for each. Web a penalty of $25,000 will be assessed on any reporting corporation that fails to file form.

Form 5471 and Form 5472 Possible FirstTime Penalty Abatement Hone

Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, with no maximum. Generally, an fta can provide penalty relief if the taxpayer has not previously been required to file.

Form 843, Claim for Refund and Request for Abatement IRS Fill

Web the annual deadline for filing both form 5471 and form 5472 is the due date of a taxpayer’s income tax return (including extensions). Web penalties systematically assessed when a form 5471, information return of u.s. When taxpayers have no unreported income and the only missed requirement was an international reporting form, it used to be the penalties. Form 5471.

Tax Offshore Citizen

Generally, an fta can provide penalty relief if the taxpayer has not previously been required to file a return or has no prior penalties (except. The penalty also applies for failure to. Form 5471 must be filed by certain. Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional.

Corporation (I.e., A Corporation With At Least One Direct Or Indirect 25% Foreign Shareholder.

Web in order to obtain an abatement of the penalties associated with a form 5472 penalty, it must be established that the individual that was assessed a penalty did not only act with. Generally, an fta can provide penalty relief if the taxpayer has not previously been required to file a return or has no prior penalties (except. I also swear and affirm all. Web the annual deadline for filing both form 5471 and form 5472 is the due date of a taxpayer’s income tax return (including extensions).

Web Use Form 5472 To Provide Information Required Under Sections 6038A And 6038C When Reportable Transactions Occur During The Tax Year Of A Reporting Corporation With A Foreign.

Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, with no maximum. The irm clarifies that relief. Web a failure to timely file a form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues,. Persons with respect to certain foreign corporations, and/or form 5472,.

Web The Irm Revisions Also Address Whether First Time Penalty Abatement (Fta) Will Take Precedence Over Relief Provided Under The Notice.

Web a penalty of $25,000 will be assessed on any reporting corporation that fails to file form 5472 when due and in the manner prescribed. When taxpayers have no unreported income and the only missed requirement was an international reporting form, it used to be the penalties. Web the penalty under irc § 6038a begins at $25,000, and the continuation penalty, which commences 90 days after notication of assessment, is $25,000 for each. Web the instructions for form 1120.

Corporation Or A Foreign Corporation Engaged In A U.s.

De required to file form 5472 can request an extension of time to file by filing form 7004. Extension of time to file. Get ready for tax season deadlines by completing any required tax forms today. To qualify, taxpayers must meet the conditions set forth in i.r.m.