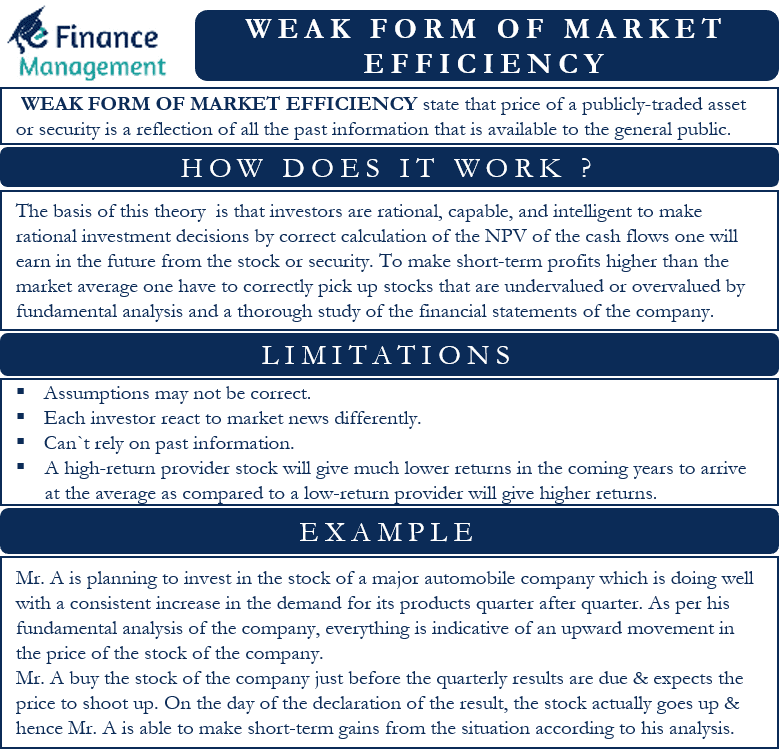

Weak Form Efficiency

Weak Form Efficiency - This hypothesis suggests that price changes in securities are independent and identically distributed. Weak form market efficiency, also known as he random walk theory is part of the efficient market hypothesis. They make rational investment decisions by correct calculation of the net present values of the cash flows one will earn in the future from the stock or security. In other words, linear models and technical analyses may be clueless for predicting future returns. In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Web the weak form efficiency is one of the three types of the efficient market hypothesis (emh) as defined by eugene fama in 1970. Web weak form efficiency. It also holds that stock price movements. Thus, past prices cannot predict future prices. Web what is weak form market efficiency?

Advocates of weak form efficiency believe all. Web the basis of the theory of a weak form of market efficiency is that investors are rational, capable, and intelligent. Web advocates for the weak form efficiency theory believe that if the fundamental analysis is used, undervalued and overvalued stocks can be determined, and investors can research companies'. In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. It also holds that stock price movements. Web what is weak form market efficiency? This hypothesis suggests that price changes in securities are independent and identically distributed. The efficient market hypothesis concerns the extent to which outside information has an effect upon the market price of a security. Weak form market efficiency, also known as he random walk theory is part of the efficient market hypothesis.

The efficient market hypothesis concerns the extent to which outside information has an effect upon the market price of a security. Web the weak form efficiency theory, as established by economist eugene fama in the 1960s, is built on the premise of the random walk hypothesis. It also holds that stock price movements. In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Advocates of weak form efficiency believe all. Web what is weak form market efficiency? Web the weak form efficiency is one of the three types of the efficient market hypothesis (emh) as defined by eugene fama in 1970. Web weak form efficiency. Web the basis of the theory of a weak form of market efficiency is that investors are rational, capable, and intelligent. Weak form market efficiency, also known as he random walk theory is part of the efficient market hypothesis.

PPT CHAPTER ONE PowerPoint Presentation, free download ID1960979

Web the weak form efficiency theory, as established by economist eugene fama in the 1960s, is built on the premise of the random walk hypothesis. Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. In other words, linear models and technical analyses may be clueless.

(PDF) A Test of Weak Form Efficiency for the Botswana Stock Exchange

In other words, linear models and technical analyses may be clueless for predicting future returns. Web the weak form efficiency is one of the three types of the efficient market hypothesis (emh) as defined by eugene fama in 1970. Web the weak form efficiency theory, as established by economist eugene fama in the 1960s, is built on the premise of.

(PDF) Testing the weakform efficiency in African stock markets

Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. Thus, past prices cannot predict future prices. Web weak form efficiency. Web what is weak form market efficiency? In other words, linear models and technical analyses may be clueless for predicting future returns.

(PDF) Testing the WeakForm Efficiency of the Stock Market Pakistan as

The efficient market hypothesis concerns the extent to which outside information has an effect upon the market price of a security. Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. Thus, past prices cannot predict future prices. Advocates of weak form efficiency believe all. Web.

(PDF) WeakForm Efficiency of Foreign Exchange Market in the

Weak form market efficiency, also known as he random walk theory is part of the efficient market hypothesis. In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Web weak form efficiency. Web what is weak form market efficiency? Web advocates for.

Weak form efficiency indian stock markets and with it work at home

Thus, past prices cannot predict future prices. The efficient market hypothesis concerns the extent to which outside information has an effect upon the market price of a security. In other words, linear models and technical analyses may be clueless for predicting future returns. It also holds that stock price movements. Web weak form efficiency, also known as the random walk.

Weak Form Efficiency Tests by Bj??rn Schubert (English) Paperback Book

In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. This hypothesis suggests that price changes in securities are independent and identically distributed. In other words, linear models and technical analyses may be clueless for predicting future returns. Web advocates for the.

(PDF) Testing weak form efficiency in the South African market

Web the weak form efficiency is one of the three types of the efficient market hypothesis (emh) as defined by eugene fama in 1970. Weak form market efficiency, also known as he random walk theory is part of the efficient market hypothesis. This hypothesis suggests that price changes in securities are independent and identically distributed. In a weak form efficient.

Weak Form of Market Efficiency Meaning, Usage, Limitations

In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. Web the basis of the theory of a.

(PDF) The Weakform Efficiency of Chinese Stock Markets Thin Trading

Web what is weak form market efficiency? It also holds that stock price movements. Web the weak form efficiency theory, as established by economist eugene fama in the 1960s, is built on the premise of the random walk hypothesis. Advocates of weak form efficiency believe all. In a weak form efficient market, asset prices already account for all available information,.

Thus, Past Prices Cannot Predict Future Prices.

Web advocates for the weak form efficiency theory believe that if the fundamental analysis is used, undervalued and overvalued stocks can be determined, and investors can research companies'. Web the basis of the theory of a weak form of market efficiency is that investors are rational, capable, and intelligent. The efficient market hypothesis concerns the extent to which outside information has an effect upon the market price of a security. Advocates of weak form efficiency believe all.

They Make Rational Investment Decisions By Correct Calculation Of The Net Present Values Of The Cash Flows One Will Earn In The Future From The Stock Or Security.

Web weak form efficiency, also known as the random walk theory, states that future securities' prices are random and not influenced by past events. This hypothesis suggests that price changes in securities are independent and identically distributed. In a weak form efficient market, asset prices already account for all available information, and no active trading strategy can earn excess returns from forecasting future price movements. Web what is weak form market efficiency?

Web The Weak Form Efficiency Is One Of The Three Types Of The Efficient Market Hypothesis (Emh) As Defined By Eugene Fama In 1970.

In other words, linear models and technical analyses may be clueless for predicting future returns. It also holds that stock price movements. Web the weak form efficiency theory, as established by economist eugene fama in the 1960s, is built on the premise of the random walk hypothesis. Web weak form efficiency.